Weather phenomena, trade headwinds and currency fluctuations could disrupt the global food price environment during 2018, according to research from Rabobank, the specialist food and agribusiness bank.

There is currently as much as a 75% chance of La Niña conditions strengthening and lasting the northern hemisphere winter, according to the US-based National Oceanic and Atmospheric Administration. The phenomenon could bring extreme heat and dryness to grain areas in the Americas and flooding to Asia’s palm oil plantations.

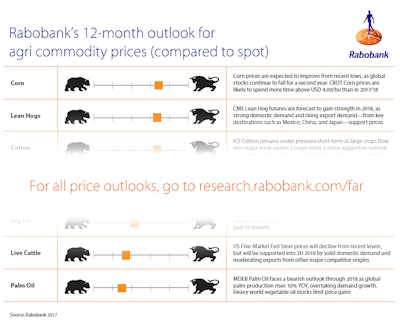

In its annual Outlook report, Good Buy, Low Prices, which analyses prospects for 13 agricultural commodities, Rabobank says that while global stocks are historically well-supplied, balance sheets are tightening, exacerbating the potential impact of shocks.

Alongside weather, other factors pose a risk to the stability of global food prices, according to Rabobank.

Trade is set to continue to play a key role in price volatility. Global freight costs – in the form of the Baltic Dry Index – and oil prices are both rising and there remains uncertainty over US policy towards NAFTA and the UK’s future trading relationship with the EU and other nations.

In currencies, the prospect of further interest rate increases in the US raises the chances of the dollar appreciating, making American exports of key commodities such as wheat and soybeans less competitive.

Stefan Vogel, head of agri commodity markets at Rabobank and report co-author, said: “Historically speaking, the global stocks of grains and oilseeds are high, which is currently keeping the pricing environment relatively benign. But there are clouds of uncertainty on the horizon and supplies are not enough to sustain prices should a major event like La Niña disrupt major agricultural areas, such as the US and South America.

“This has the potential to cause a supply shock that would ripple through to food prices, while the rising cost of global trade and potential currency fluctuations also create upside risks. Our view is these outweigh the downside risks in 2018.

“Producers must therefore guard against complacency after years of relative stability and plan ahead to manage these risks proactively and appropriately.”

Among individual commodities, Rabobank expects global demand for coffee to continue to grow, leading to a slightly bullish view on 2018 prices despite a potential 3m-bag surplus in 2018/19. Demand for cocoa also continues to rise, driven by developing nations’ taste for luxury commodities, though large global stocks mean price spikes are unlikely.

The outlook for wheat is bullish relative to today’s prices due to an expected 7.5m-tonne global deficit (excluding China), driving a trend towards rebalancing after record-low planted acres in the US this year.

Stefan Vogel added: “As ever, various factors are at play when looking at prospects for next year, but in the case of coffee and cocoa, prices are supported by rising demand for these luxury commodities, particularly from emerging markets.

“Nevertheless, the picture is mixed elsewhere, with demand for wheat tempered by large supplies and record stocks, while palm oil producers are challenged by the need to reclaim market share from other oils given adverse weather has hit yields since 2015/16.”

The annual Outlook report, now in its eighth year, is produced by Rabobank’s specialist team of agricultural commodity markets researchers based around the world.